|

A Guide to Implementing the Theory of

Constraints (TOC) |

|||||

Evaluating Change When we set out to implement

change we must remember that there are 3 possible outcomes. These outcomes are; (1) A

change which is a significant improvement. (2) A

change which is neither a significant improvement nor a significant decline. (3) A

change which is a significant decline. Naturally enough, it is

the first option that we are really seeking.

We want to make a difference, and we want that difference to be

manifestly positive. In order to do

so, we must make decisions prior to carrying out the desired actions, and to

be certain in the knowledge that those decisions will deliver the necessary

results that we seek. How we evaluate the

improvement will depend upon the goal of the system. If the goal is a monetary one, then the

evaluation is relatively straightforward.

And that is what we will concentrate on here. In not-for-profit, or more correctly,

for-cause situations how we evaluate an improvement is a little more

involved; however, if you look at the argument for healthcare (supply chain

section) then you will find some good indications of how this can be

achieved. We are evaluating changes

within the context of the whole system – or the system as a whole. We are not interested in local improvements

that do not have system-wide impact.

How, then, would we judge an impact in such a circumstance? We need a context. We already have one, let’s revisit it. On the measurements page

we derived our rules of engagement.

These tell us how to define the entity that we want to improve. We define the boundaries, the goal, the

necessary conditions, and the fundamental measurements. Without these, we do not have a context

within which to evaluate change.

Moreover, this forces us to determine what it is that constrains us

from moving towards our goal; we have to define the role of the constraints. The constraints are

central to our ability to move forward.

In order to define the role of the constraints we need to invoke our

plan of attack, the one we developed on the process of change page. Of course, our plan of attack is Goldratt’s

focusing process. The second step of

this plan, where we decide how to exploit the constraints, is the step that

provides commonality between these two schemes. We have previously

summarized the relationship between the rules of engagement and the plan of

attack as follows;

In order for a change to be

an improvement it must either have a direct positive effect upon the current

exploitation or elevation of the system’s constraints, or an indirect effect

via improved subordination which in-turn ought to improve the exploitation or

elevation, either now or in the future.

To quantify these effects

we must return to our fundamental measurements. In the first page, the

page on measurements, we briefly introduced the concepts of; throughput, inventory/investment,

and operating expense; a triumvirate set

of measures for quantifying effects in Theory of Constraints. Throughput as you may

remember was described as; Throughput

= Sales - Totally Variable Costs From this we came to

define our net profit as; Net Profit

= Throughput - Operating Expense And return-on-investment

is;

The reason that we can do

so much with so little is because of the fundamental relationships that exist

between each measure. They are systemic. Let’s try to reinforce

the fundamental and systemic nature of these measures by way of analogy. By this means we will be in a far stronger

position to understand change and how to evaluate it. The analogy is a see-saw. A see-saw!

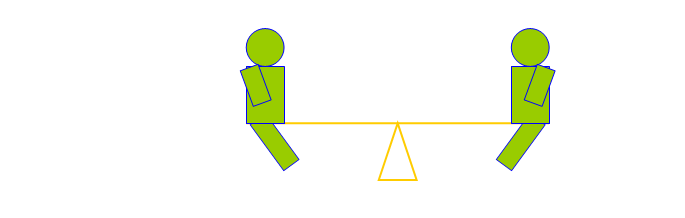

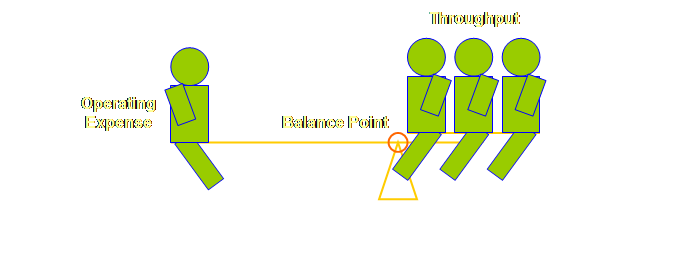

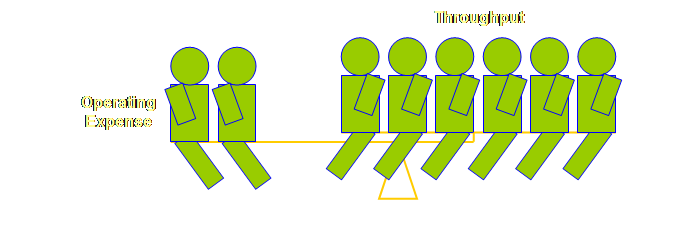

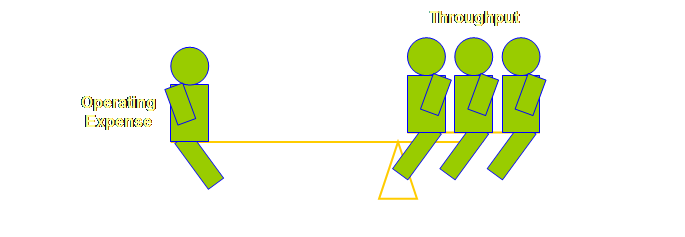

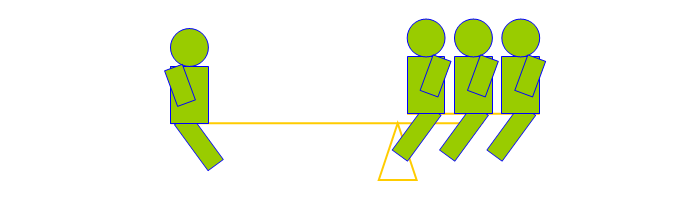

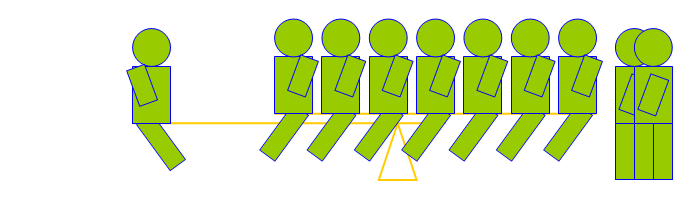

How does the evaluation of change relate to a see-saw? Well, let’s have a look. Let’s draw a simple see-saw as a start.

The two equal masses – “people” are located

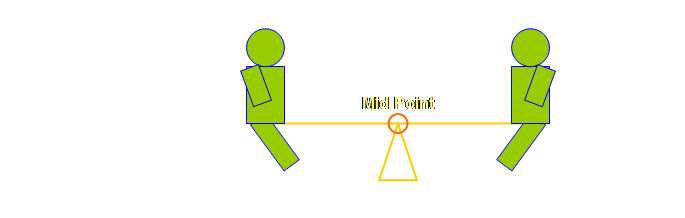

equidistant from the mid-point of the plank, so let’s label that.

Let’s see.

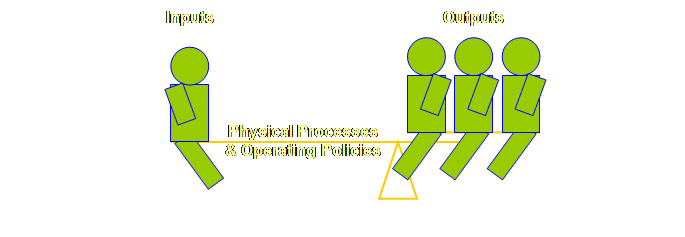

Can we use this simple analogy of a see-saw for

evaluating internal management decisions, change in other words? In terms of physical

aspects it is apparent that we seek to leverage inputs of some

kind via a process of some sort in order to produce outputs. In fact, the process does not exist in

isolation but rather it exists in conjunction with a set of operating

assumptions; the things that we call policies. How then would this look using our

model? Let’s see.

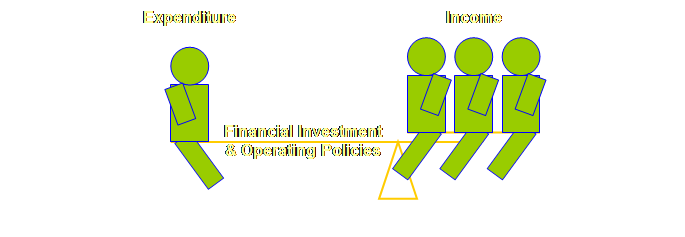

How then would our model look in terms of financial

aspects? In the terms of financial aspects it is apparent that we seek to leverage

expenditure via investment to produce income.

Once again the investment does not exist in isolation but rather it

exists in conjunction with a set of working assumptions; policies once

again. Let’s see how this looks.

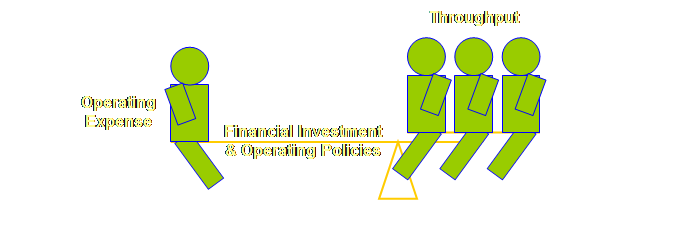

We need to ask then; will this simple analogy, a

see-saw, also work as a description for evaluating change in Theory of

Constraints? Well, I think so, so

let’s try.

It seems then, that our analogy will hold for our fundamental

measures. Great. Any change in throughput, or operating expense may

change the balance of our system. Do

you agree? Our analogy shows the

interrelationships between these various aspects. Do you want to push the analogy a little bit

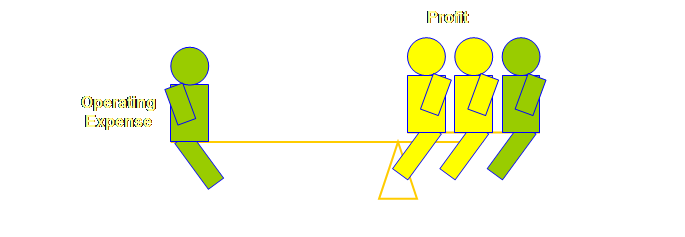

further? What is our profit then? Let’s have a look.

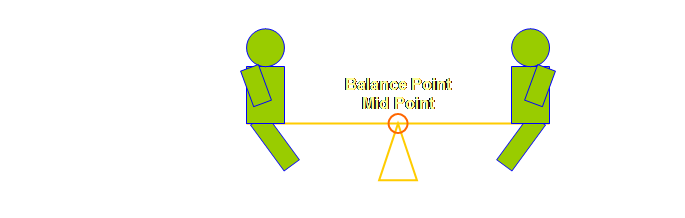

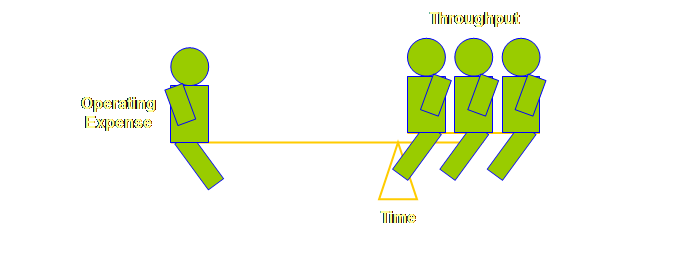

What about the balance point then?

We know the location of the balance point, but this

begs a question. What is the fulcrum

that we leverage across? Let’s have a look.

I know that all too often we loosely talk about

leveraging the constraint – we have used that language throughout these

webpages and it is probably ingrained.

But in reality we are leveraging our entire system

over the fulcrum – time – and the only

way that we can do that, either literally or metaphorically, is via the

constraint. So we leverage the

system via the constraint for a given unit of time. So, yet another question; what exactly is the

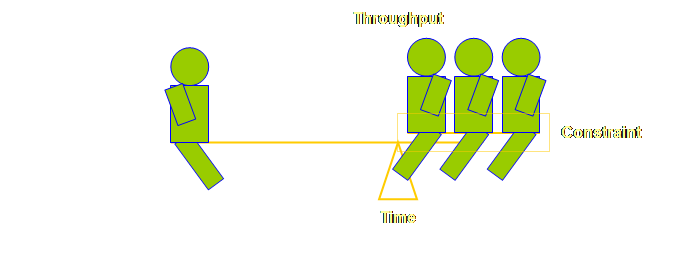

constraint in our analogy then?

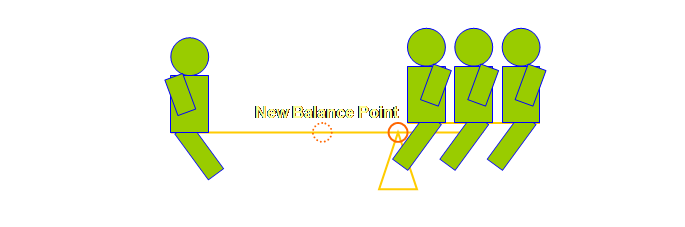

Now that we have identified

the constraint, how can we get more of this limiting factor? How in our metaphor can we get more people

sitting balanced on the right-hand side?

How can we improve the Throughput?

How can we improve the profit?

There are two answers to these questions, and they are that we can

increase the productivity, and/or we can increase the production. We need to tease these two strands apart in

order to better understand each of them.

Let’s do that. Making a distinction between productivity and

production is important in understanding how to most effectively drive

improvement, and such a distinction is also useful in developing our

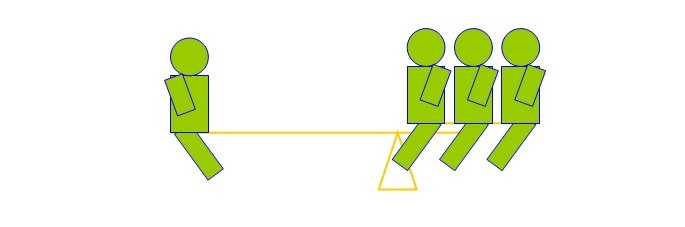

understanding of the dynamics of exploitation, subordination, and elevation. Production is the simpler, and certainly

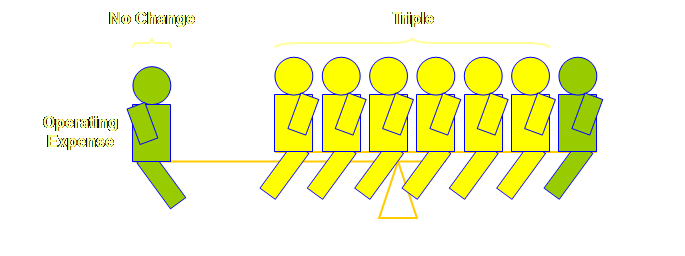

more familiar of the two concepts, so let’s start with that. Essentially any increase in production is a pro rata

increase in both inputs (operating expense), and outputs (Throughput). Let’s investigate this with our see-saw

analogy. Let’s start again with our original model with a

balance point located 3/4 of the way along the plank.

Increasing production, seductive as it is – after

all this is what almost everybody else does – is nowhere near as sexy as

improving productivity per se.

Moreover, if we were to go around doing what everyone else does then

there is hardly any strategic advantage to be had at all. So let’s investigate the impact of

improving productivity; many people talk about increasing productivity but

few actually manage to do it. Doing it

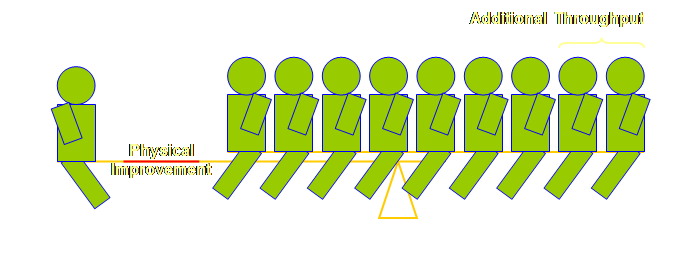

is not at all difficult if we have focus. Rather than settling for a pro rata increase in both

operating expense and throughput, which means constant productivity – only

more of it, we actively seek to decouple throughput from operating expense,

which in-turn means increased productivity.

Throughput should increase and ideally operating expense should remain

static or even decrease; something other than additional operating expense

drives the additional throughput. It

is the leveraging of the entire system via the constraint’s throughput

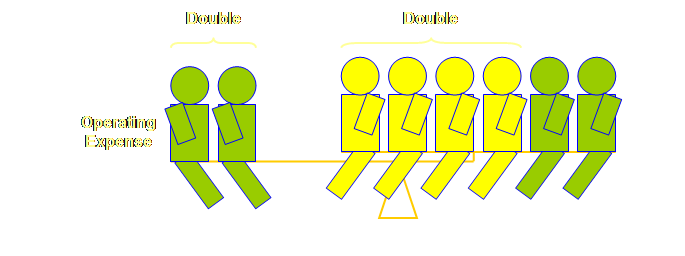

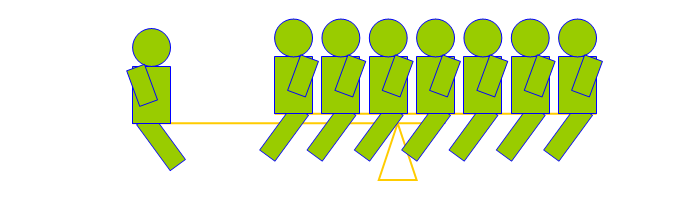

relative to the fulcrum, time, that drives the additional throughput. Let’s show this by example. Let’s start again with our original model with a 3:1

ratio.

An increase in productivity will in-turn

substantially increase profit. Let’s

have a look at that.

We obtain better leverage by better exploitation of the constraint (the secondary plank

becomes longer) and by better subordination

of the non-constraints. Often the

simplest way to obtain an increase in leverage is to remove or modify some

current policy. Organizations abound

with policy; that is, after all, one way in which to standardize matters, and

without standardization there can be no base from which to improve. But what if the standardization causes us

to stagnate instead of improve? Policy

also allows us to react quickly without reinventing the wheel each time. But what if we no longer need a particular

reaction and yet we still have the policy?

Removal of outdated or inappropriate policy unblocks access to current

capacity and increases productivity. Now, if we are still bored with our newfound

increase in productivity, then we can still increase our production after we have increased our productivity – given that our

capacity allows for it. It pays in

more ways than one to increase relative productivity first, and then absolute

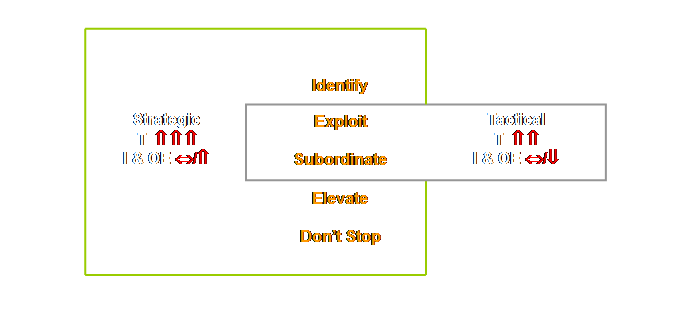

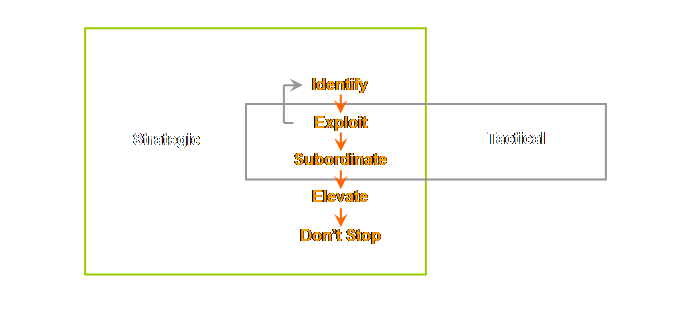

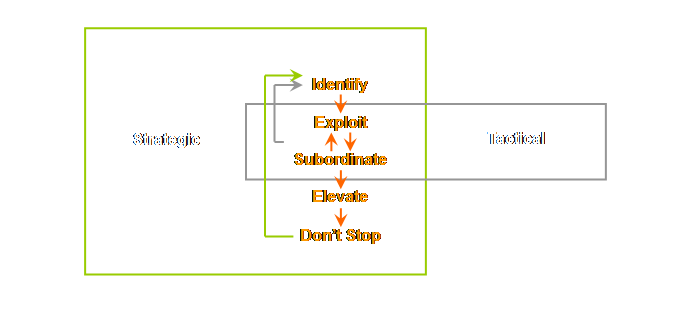

production second, rather than the other way around. Always aim for capability before capacity. That is why the 5 focusing steps; our plan of attack

goes; identify, exploit/subordinate, elevate

– in that order. Most firms go;

identify, elevate – every time. In

fact that is unfair, most firms miss the identification stage and have a

scatter gun approach of; elevate, elevate, elevate. Hardly a wise use of cash, and a total

absence of any systematic decision analysis. In reality, often both productivity and production

are inexorably mixed together, but we need to understand the dynamics of each

component if we are to better understand how to correctly influence the whole

– even if later on we can’t so neatly break the whole back into constituent

parts as we have here. It is apparent from the logic of this discussion

that as the lever moves with respect to the fulcrum; the productivity, throughput,

and hence profit, should trend towards infinity. But we are getting ahead of ourselves. None of us are making infinite profits yet

(or if we are, then we certainly haven’t told Inland Revenue about it). So, this begs a question. Why aren’t we making infinite profits yet? Well, a valid reason might be a finite

capacity or capability of the current constraint; we are unable to move the

balance point any closer to the end of the lever. We can neither exploit the constraint nor

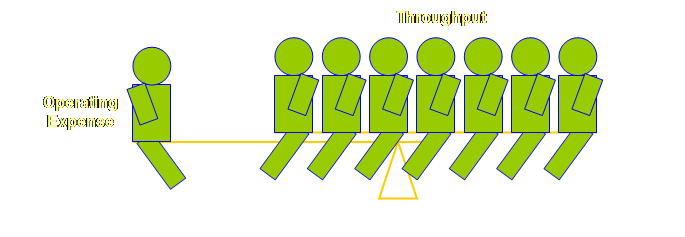

subordinate the system any further, even though the demand is there? What shall we do? Well, why don’t we make the lever even longer? Let’s have a look at a new aspect;

investment. In our analogy additional investment means that our

lever becomes a little longer. The

effect of the investment in this instance is to both exploit

& elevate the existing constraint or to better subordinate the

non-constraints which in-turn exploits the constraint. Let’s work from our current state where we

have 7/8’s of the lever on one side and 1/8 on the other. Here is our starting point.

The effect of the investment is to increase the

physical leveragability of the system even though the absolute position of

the balance point remains static.

Effectively we have increased the productivity of the system by

capital investment. This is

interesting (to me). Here we have both

elevation (cash from outside the

system was brought inside – even though it is not an increase in operating

expense) and exploitation (the absolute

position of the balance point did not change, but the position relative to

the whole plank did change). Alright, maybe that is pushing our metaphor

about as far as it should go at the moment. Let’s now return to the formulae that express the

reality of these simple diagrams to further evaluate the situation. We introduced 3 equations in the section on

fundamental measurements, let’s repeat two of them here, one for throughput

and one for profit (or operating surplus); Throughput

= Sales - Totally Variable Costs and Net Profit

= Throughput - Operating Expense Of course we can combine these into one statement Net Profit

= Sales - Totally Variable Costs - Operating

Expense However, let’s confine ourselves to the simpler

version Net Profit

= Throughput - Operating Expense And let’s compare this directly with the simplest of

our see-saw analogies. Here is the

analogy.

Net Profit = 3 Units of

Throughput - 1 Unit of Operating Expense

= 2 Units Just as we drew it,

We can see that the fulcrum is represented in the

diagrams and we can see that its positioning under the balance point is

critical, and we know that it represents time, yet it seems to disappear from

our equations. Let’s clarify this

issue. The fulcrum is time – the one thing we don’t seem to

be able to generate any additional quantity of, and time is present in our

equations, but we seem to have been a little lax in making it explicit. Really our equations should read as

follows. Throughput should be;

And one again, if we combine these equations we get;

We are more interested in evaluating change before

we make the change. We want to know

the outcome of a potential decision before we take action to implement it as

an actual decision. And for this we

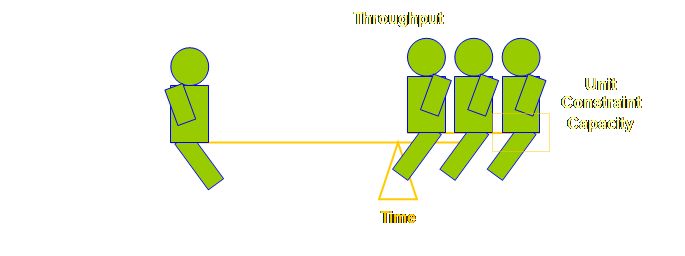

need some critical information. We need to be able to determine the Throughput

through a unit of constraint capacity in relation to time.

This is the major

decision analysis that we make. We

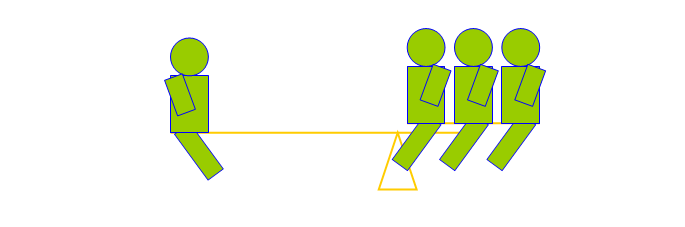

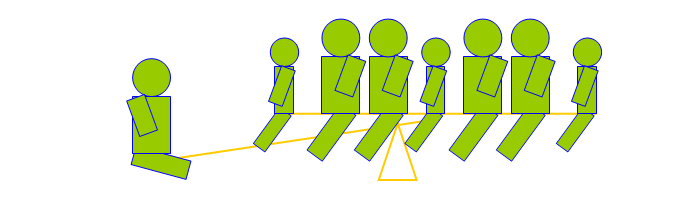

need to examine this in detail. Let’s return to our original case for a moment.

Upon the improved leverage of the example above we

found the following;

But equally, we might also have found this;

If we substituted children for all of the adults we

could even have found this;

How can we know ahead of time what the outcome of

these types of substitutions will be?

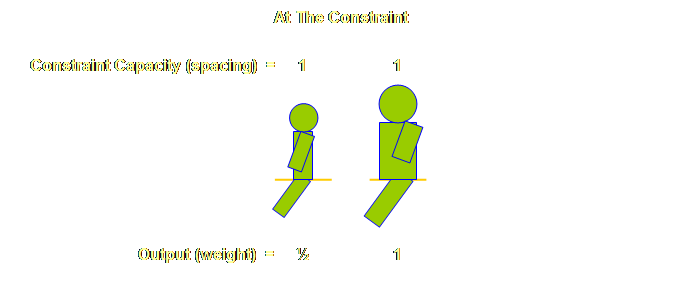

Graphically it seem obvious, we need to know the output value, the

weight, for each type of output in this system relative

to the unit constraint capacity. Let’s show this.

It is a simple step to move our analogy from output

to throughput so that we can evaluate the financial

aspects. Let’s have a look.

We have produced a normalized throughput per unit of

output as viewed from the perspective of the constraint. But, we have

nearly lost sight of our fulcrum (again).

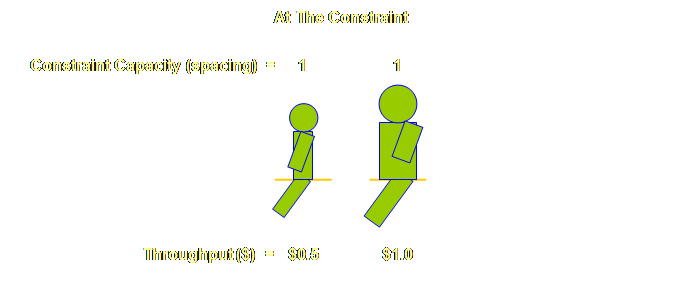

What has happened to our measure of time? Mention was made of the short-hand expression “T/cu”

or Throughput per constraint unit earlier.

This short-hand is partially responsible for the apparent lack of

time. It is there, however. The full expression should be “throughput

per constraint unit per unit time,” or T/cu/t. In our simple analogy our constraint unit is

seating, and thus we would evaluate Throughput as Throughput $ per seat per

ride. “Seat” is the constraint unit,

“ride” is the expression for time. Let’s look at a few other general cases. What about a sunshine factory? And by that I mean an outdoor agricultural

or horticultural enterprise. The

constraint unit here is available productive area, and the decision analysis

becomes Throughput $ per acre or hectare per season or per year (T$/hectare/year). What about an indoor retail operation? Something that doesn’t make anything; just

buys and sells. The constraint unit

here is again productive area, if might be square meters or square feet of

floor space, or square meters or square feet of shelf space if there is a

vertical component as well, and the decision analysis becomes Throughput $

per square meter per week or per month depending on the rate of turnover (T$/m2/week).

Supermarkets tend to use linear meters of “facing” assuming that we

buy in proportion to what we see. If

the facing all has the same volume stacked behind it, then there would seem

to be little difference in the various units. Larger items in a sales system where a sale is

concluded after a sales process, then the constraint should be the number of

contact sales hours that the sales people have. The decision analysis becomes Throughput $

per sales person per hour or day (T$/sales person/hour). In manufacturing the constraint is most usually a

machine or group of machines and this is the constraint unit, the unit of

time is most commonly minutes because manufacturing steps are more commonly

completed within minutes or hours rather than days. The throughput decision analysis becomes

Throughput $ per machine per minute (T$/machine/minute). Some examples that I know of are

people-paced rather than machine-paced and the throughput decision analysis

becomes Throughput $ per man per hour (T$/man/hour). What then of projects? The constraint is the number of resources

working on the critical chain. The

Throughput decision analysis becomes Throughput $ per critical chain person

per project week or month (T$/critical chain

person/month). Remember these are decision analyses; the analysis

of various choices before we

embark on a decision. Once we have

made a commitment to the customer we can’t internally re-prioritize according

these values. With this new information under our belt, now, at

least, we can predict the Throughput for the following case before we

actually do it.

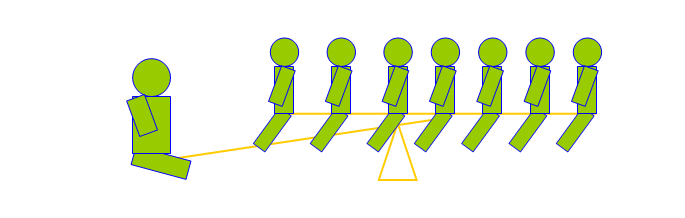

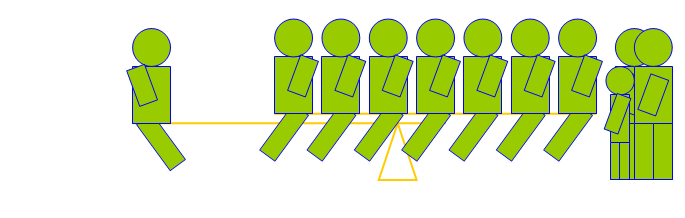

What about the other case?

Graphically this is just plain obvious, we can see,

and we know from our own direct experience with see-saws. But trust me, in most organizational

systems this is anything but clear, and one good reason for this is that

almost no one in most organizations has ever considered this before. “We have to evaluate the impact, not of a product,

but of a decision. This evaluation

must be done through the impact on the system’s constraints. That’s why identifying the constraints is

always the first step (1).” We have to know

where the constraint, is; and we have to know

the Throughput value of the output with respect to that constraint. So, anyone can

work out the Throughput retrospectively for any period. No one can

evaluate the Throughput proactively for the current or future periods without

explicit knowledge of the Throughput value generated with respect to the

constraint. In some instances this

might be quite obvious; most often, however, it is not. And when it is done there are most often

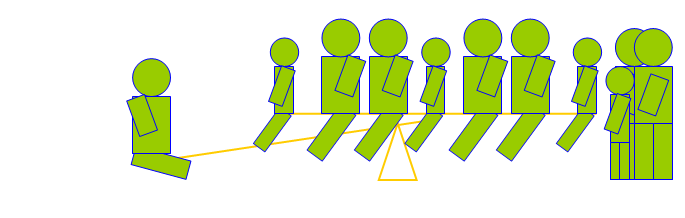

some surprises in the relative ranking of the outputs. This brings us to a very important point. We all know from our own personal experiences with

see-saws, that if we change just one important thing then the whole balance

may change. If we move the plank a

little, or if someone gets on, or if someone gets off, or even it someone

changes ends, then, so too, does the balance.

And so too, with our system under investigation. We didn’t know previously that once we elevated this

system that children might get on, or that adults might get off. But every time we prepare to change the

constraint that is exactly what we must evaluate for. We must evaluate for the new mix that could

arise. If we think that we will

elevate a constraint to the extent that we will break it (and thus a new

constraint presents itself) then the unit throughput values, and thus the

individual ranking, may also change and therefore maybe also our tactics for exploitation

will change as well. We must predict the outcome ahead of implementing

the decision. “You see, in the ‘cost

world’ almost everything is important, thus changing one or two things

doesn’t change the total picture much.

But this is not the case in the ‘throughput world.’ Here, very few things are really

important. Change one important thing

and you must re-evaluate the entire situation (2).” In internally constrained systems we can not satisfy

market demand. We can show this with

our analogy? Of course we can. The beam is full, we could get other people

on, if only they would fit.

We have, loosely speaking, begun to evaluate

decisions about the composition of the physical output – the so-called

production mix. Now, there is almost

nothing, either positive or negative, that a good production manager can not

ascribe, in one way or another, to the changes in the production mix. The production manager can do this without

fear of contradiction because, in fact, almost no one else understands the

true impact of the production mix – often not even the production manager! But we do understand – only too well. We do, because we know how to strip out all of the

raw material costs or 1:1 variable costs in the production mix leaving

us with the bare essentials – we could call this the throughput mix

(3, 4). Moreover, we know that we must

evaluate the throughput mix in relation to one thing and one thing only, the

amount of resource consumed to produce the throughput mix on the constraint. Let’s therefore look at this in a little more

detail. We need to better delineate

some aspects that are particularly important in internally constrained

environments. Maybe we should describe

these as generic tactics. We need to do this in order to later

appreciate some of the subtle changes that occur in the tactics once a system

becomes externally constrained. It becomes part of the exploitation strategy of

internally constrained systems to maximize the throughput mix by including,

as much as possible, products that generate high throughput per unit time on

the constraint; these are the adults of our analogy. In shorthand we might describe these as

high “T/cu” products, where “T” means throughput and “cu” means constraint

unit. We saw this aspect demonstrated

so well in the P & Q analysis. However, I want to introduce the word “grade” to

describe this aspect of throughput mix.

We want to substitute, wherever possible, higher grade unit throughput

for lower grade unit throughput. We

want to produce “stars” not “dogs” if the market will allow us – and it

should. The overall grade is a

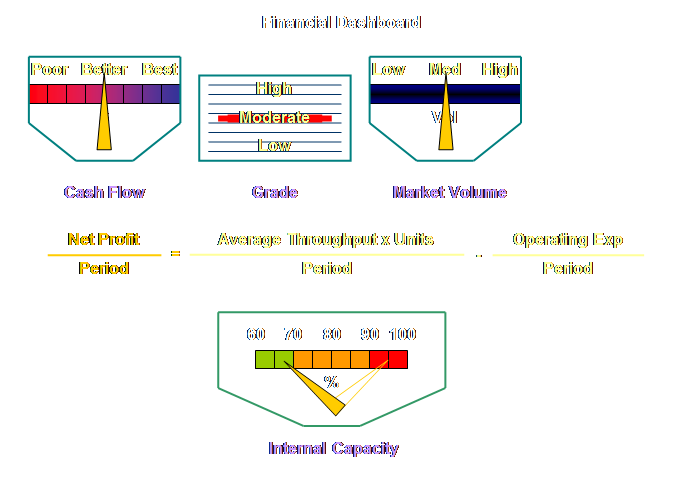

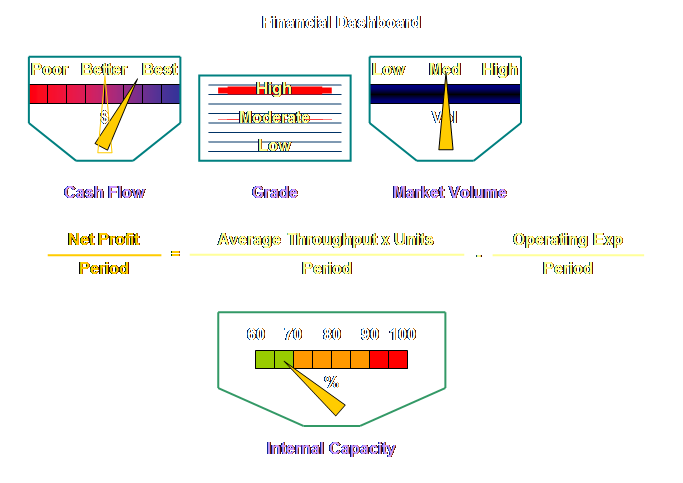

reflection of the average throughput per unit. Moreover, let’s call the current market capacity

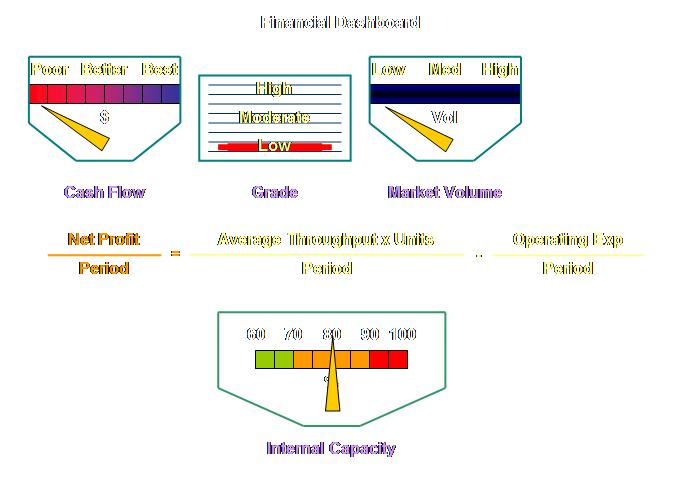

“market volume” and the profit “cash flow.”

Let’s have a look at the relationships.

And I would like to embellish this further – or at

least make it easier for me to understand – by adding some “gauges” to this;

a sort of metaphorical dashboard for our system. And let’s assume for the moment that this

is the view prior to implementing our new-found knowledge.

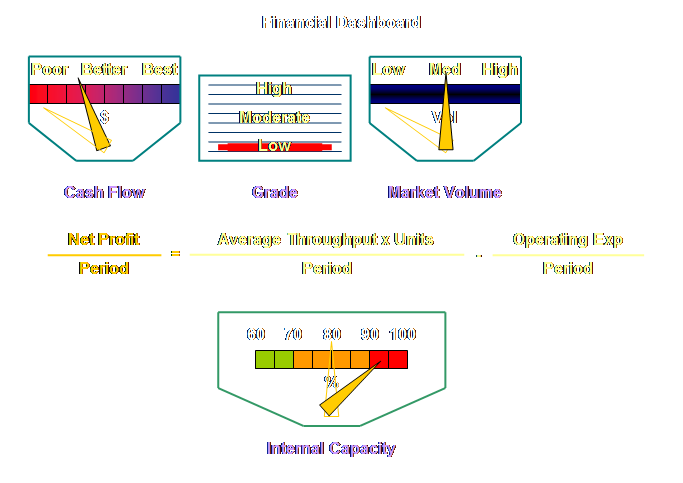

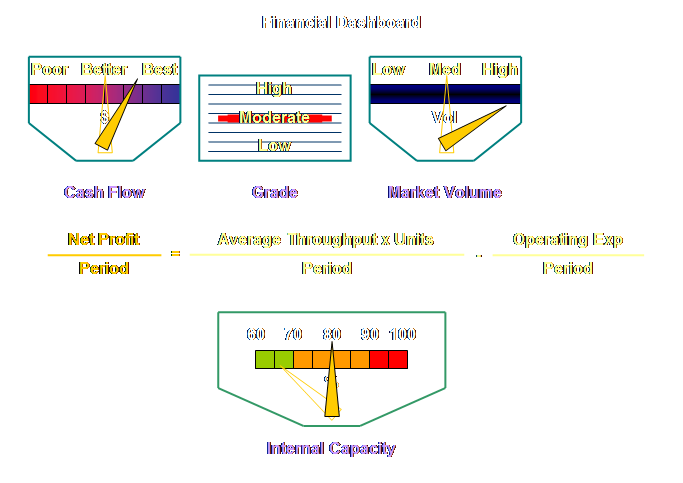

Therefore, let’s exploit this internally constrained

system and see what happens.

This is a way of showing that in an internally

constrained system it is the Throughput grade that

is most important in raising the net

profit of the system. If you can

actively substitute high grade products for low grade products in any new

orders, then you will improve your cashflow. Now a question; is this active substitution an

example of exploitation or of subordination? My answer to that is both! We further exploited the constraint (and

therefore the system as a whole) by subordinating our output decisions in

order to maximise the throughput grade.

However, do we want to stay in this zone, the red zone of our constraintometer? Shouldn’t we try to bring the operation

down, or rather the capacity up, into the green zone? In essence we are beginning to tread into

an area where we need to distinguish between tactical and strategic

decisions. There is no need to tread, let’s rush headlong in! In our evaluation decisions we are essentially

asking what effect an actual action now, or a potential action in the future,

has upon our profit and/or our return on investment. These, after all, are our measures of

success in a for-profit organization.

We need to know whether the change is a significant improvement or

not, and if so, the magnitude of the improvement as well. However, we can also examine these actions from

another viewpoint – whether they are tactical or strategic in nature. I will suggest that net profit is largely a

tactical decision; how can we best maximize the return on our current

assets. Return on investment is

largely a strategic decision; how can we best maximize the return on any

additional assets. It’s not a clear

cut dichotomy, but it may be useful nevertheless. We can place this distinction within the framework

of our plan of attack, our 5 step focusing process. Let’s show the generalized effect on

throughput (T), inventory/investment (I) and operating expense (OE) within

this framework.

Let’s now consider the steps identify and

elevate. When we elevate a constraint

we most often bring additional investment into the system, usually in the

form of the purchase of additional capacity.

We may also need to increase operating expense in order to utilize the

new capacity. Thus inventory

(investment) will increase and operating expense will most likely increase

also, if only due to the increased depreciation of the new investment. Because investment is most often required

at these stages, let’s suggest that this is a strategic decision. Both tactical and strategic decisions should have a

positive impact of the productivity of the system. This is easy to determine for

non-investments. But the moment we

make an investment it is no longer straight forward. Investments are apparently invisible to our

definition of productivity;

Of course neither tactical nor strategic decisions

should be passive – determined by the next accidental emergence of a new

constraint. They should be the result

of active analysis of where we want the constraint to be. After all, the location of the constraint

dictates the way in which our firm will make money – and where our capital

investment, product development, marketing and sales efforts will be. Sometimes where there are

significant cost/capacity differences across the system we may find that the

constraint becomes by default; (1) the

most capital intensive step in the process (2) the

most capacity extensive step in the process and this is the least

likely to be overcome anytime soon because of; (1) direct

cost in the case of the most capital intensive step (2) indirect

costs of bringing up sufficient sprint capacity in the non-constraints for

the most capacity extensive step. The subdivision of whether

something is tactical or strategic based upon external investment is a useful

distinction; however, often substantial improvement can be obtained without

additional investment at all. In fact

during this tactical phase questions of strategic importance will occur. So, let’s not be mislead into believing

that constraints are only broken by elevation. Often, especially in the earliest stages of an

implementation, proper exploitation may be all that is required to break an

apparent constraint and to expose a new constraint somewhere else in the

system. Let’s call this an immature

stage and let’s try and draw it.

We can also break an apparent constraint simply by

proper subordination. Consider in

manufacturing where non-constraints may be regrouping separately scheduled

process batches together again – insubordination in fact (pun intended). This will actually slow the whole process

down and if it occurs in one area – maybe near the gating operation for

instance then it may manifest itself as an apparent physical constraint

somewhere else within the process. The

other extreme might be when sprint capacity is beginning to be eroded due to

increased output, constraints will appear to be “breaking out” in various

places – however the solution is to increase the buffer size. Really the constraint in both cases is in the

inertia of our subordination policies.

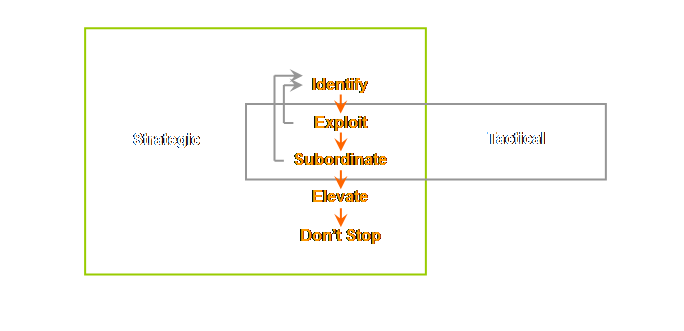

We can “short” the loop once again; identify-exploit-subordinate-identify.

Let’s add this.

In more mature implementations however the dynamic

is a little more constrained. In more

mature implementations there is a strong interrelationship between

exploitation of the constraint and subordination of the non-constraints. Breaking a constraint is more likely to

arise out of this interaction than either exploitation or subordination

alone. Let’s show this.

If the location of the constraint dictates the way

in which our firm will make money, or the way in which our organization will

make output, we may in fact have a preferred place for the constraint to

be. It may remain in the same place

for long periods of time; both static and strategic. Too often at first we are confused by our

prior experience and the notion that bottlenecks “wander” or “pop up.” We can control the process if we want to. In fact we must. Sometimes the methods of evaluating change are

derided as short-term by those who do not understand their strategic

significance. Sometimes too, the

focusing process, our plan of attack, is considered a short-term tactical

methodology. Both interpretations are

shallow and impoverished. There is a special richness in the focusing process

that is lost on many people – after all it is not exactly explicit about

it. Others, however, have gone to

considerable lengths to highlight this richness; often supplementing new

words into the scheme. The strategic

nature of the focusing process is important.

If you are especially comfortable with this concept, or more so if you

are especially uncomfortable with this concept, then at some time in the

future please come back for an extended discussion here. Ultimately, however, if we keep elevating our

internal constraint – even if we choose to keep it in one selected place –

then at some time we will move the constraint into the market. Many argue that this is exactly where it

should be. Theory of Constraints had its genesis in internal

capacity constrained systems. A great

deal of the early literature deals with this exclusively. Sometimes then, there is a disjoint as we

start to deal with external constraints.

I don’t believe that this disjoint exits in reality, I think that it

is symptomatic of the history and some inertia in terminology as we move out

from an internally constrained environment that is within our span of control towards an externally constrained

environment that is often only within our sphere of

influence – or so we like to think. Because we won’t touch upon this again until the

supply chain pages let’s be sure to understand that even though the constraints may now be external, the solutions are always internal.

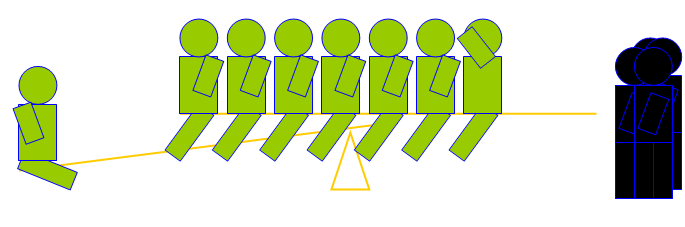

Otherwise, how else could we ever bring about the solution? Let’s return to our see-saw analogy once again, and

continue from where we left off with an internally constrained system where

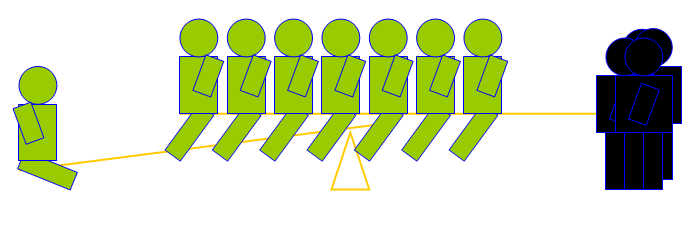

one unit of operating expense can leverage 7 units of throughput.

How then do we evaluate change in this new

circumstance? Our constraint has now

disappeared off into the market; the constraint has become nebulous rather

than physical. To answer this question we need to just slightly

reframe the situation. Sure, the

constraint is now in the market, but ask yourself, where is the internal

weakest link? It’s still back in the

physical process somewhere; most likely exactly where we last left it. Let’s have a look.

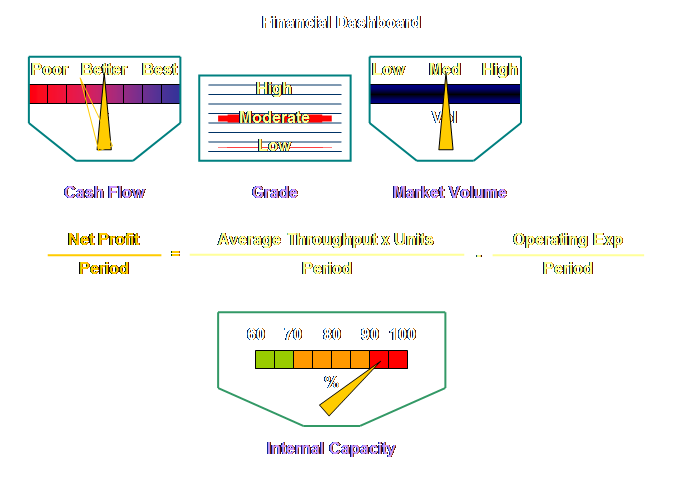

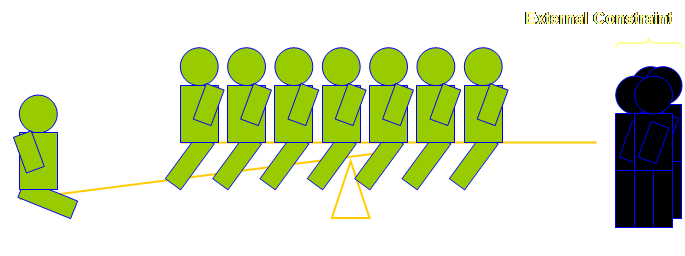

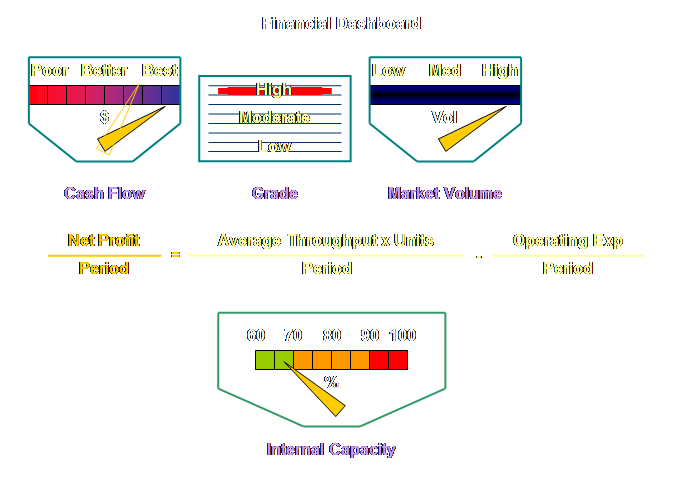

Back to our

dashboard. How has it changed since we

last left it?

However, too often this is exactly

where the disjoint occurs. You see we have two pathways down which we

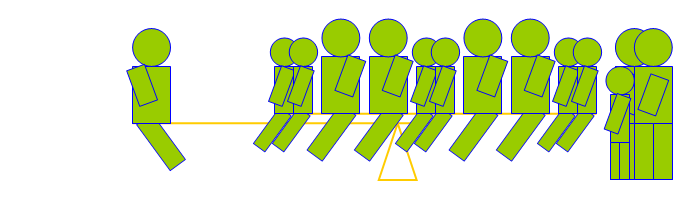

can travel. The first is to increase

loading on the internal constraint.

Let’s have a look at this.

What then of the other

pathway?

Let’s have a look.

You know, we spend so

much time and effort exploiting the financial advantage of an internally

constrained system (because we have no choice) and then the moment that it

becomes externally constrained we suddenly discontinue to properly exploit

the financial advantage (because now we have a choice), and we so often

decide to accept volume instead of grade because for maybe the very first

time we can accept volume. I’m afraid that this

won’t do, not if we have a strategy. We press the issue when

we have an internal constraint that the sales people must be aligned with the

value that the constraint can produce.

We don’t waste valuable and limited constraint capacity on goods of

lower value when we can move goods of higher value, and by definition we

can. This is, after all, a central

part of our exploitation tactic. It

shouldn’t be any different when the capacity has risen to such an extent that

the constraint is now external to the system unless there are issues about

solvency. When we were internally

constrained, the grade of the earnings were paramount because in fact we

couldn’t affect the cashflow in any other meaningful way. Does this change now? Do we send our sales people out with instructions

that any additional dollar is a good dollar just because additional volume is

now an option? Heck no! We just trained them. OK “trained salesman” is an oxymoron;

rather, we just got them aligned with one set of ideals, then we throw that

out and bring in another? I don’t

think so. We are after both dimensions now, not just one or the other. We want both the best grade of Throughput

as determined the internal weakest link and the most volume of

Throughput as determined by the capacity of the external marketing

constraint. To put it bluntly; we are

after the “fat guys.”

We get them on the see-saw by changing our

policies. Our system will still

contain some policy issues that stop our customers from buying our goods;

moreover, our system will still contain some policy issues that stop our customers

from paying more for the same goods.

This is because we fail to explain to our customers (and our

salespeople) how our value delivers real additional value to them. We have to surface and remove these policy

issues. If you like, we elevate the

system by extending a policy plank, a policy extension, call it what you

like; it most probably will cost us nothing but it will substantially improve

the profitability of the organization. It seems odd to say it, but we must; we can’t

evaluate change without a strategy. It

seems odd because so often we infer that a strategy exists – our personal

interpretation of what we deem the strategy to be. However, we must make sure that we all know, understand, share, and

are aligned with the same strategy

– implicit or explicit. We simply

can’t evaluate a local tactic without knowing the overall strategic

intent. To develop this notion

further, let’s return to our analogy one last time. Remember when we had a mix of adults and children on

the see-saw, each occupying an individual position?

What if the strategy had been to develop “thrills

for mature adults?” Then surely we

might risk future success by having too many children on-board. What if the strategy had been to develop “a fun

environment for children?” Then having

too many “old” people around might equally risk future success. What if the strategy was “good value family

fun?” Then the current tactic might be

perfectly acceptable. And maybe, just

maybe, we could have protected our throughput too. Consider the following;

But the more important point is we can’t evaluate a current tactic without knowing the

strategy. And therefore we can’t

evaluate change without knowing the strategy. Sure, we started with a context, our rules of

engagement, but this is insufficient.

It is necessary to go one level deeper below

the necessary conditions and the

goal. We need to know the next layer

down, this is the first place where a "strategic intent" becomes

apparent because it is the first place where non-generic company-specific

objectives can occur. Dettmer terms

these first several layers below the goal “critical

success factors” in his Constraints Management Model for Strategy

(7). We will cover this model in more

detail in a page of its own. In a for-profit organization, regardless of whether

we are currently internally constrained or currently externally constrained,

we must ask if we will we accept any sale that has a throughput that exceeds

the raw material cost or the 1:1 variable cost? This is not a trick question. We think that we know the answer when we

are internally constrained – at least in theory – because we know how to

maximize the throughput on the constraint by adjusting the mix. But even there we have to have an eye to

the future and the overall strategy. More importantly, because the answer is less clear,

we need to know what happens in an “external” market constrained

situation. If for example our market

is constrained; we can make several sales with a low grade Throughput now,

and one sale with a high grade Throughput.

This isn’t a problem now, but it might be in the future. It might be if our market thinks that we

are a supplier of low grade Throughput goods or services. We need to ask would we knowingly forgo a

larger and on-going Throughput in the future in order to secure a smaller

Throughput now? Forget about discounted cash flow, just use common

sense. The answer is no! Well, the answer is no, unless cash is the most

important thing, which is to say that immediate solvency is such an issue

that there might be no future unless we address the “now” both quickly and

effectively. But really this is an

issue for solvency practitioners. So, accepting a low grade Throughput now for most

firms is trading short-term gains against long-term success. It is a local

optimization in time. We trade a short-term, hopefully one-off,

and local benefit for long-term, on-going, and global benefit. Why, why, why, do we do this to ourselves? We move away from local optimization in

space in our process – and to be frank we are usually overwhelmed by the

improvement – and then we completely fail to remove local optimization from

time. Why is this?

Any ideas? Could it be impatient investors? Unhelpful institutions? Our cherished Christmas bonus? Pressure from wage rounds? The local council or municipalities’ new

rate structure? Hell no, the goal of

our business isn’t to furnish cash to ever-increasing rate demands, is it? Could these be excuses? Excuses for the lack of something. Excuses for the lack of an actual strategy. Really, that is still too superficial; it is really

the lack of understanding or belief in a strategy. And we are not talking about a plan or an explicit

document – we have all seen those. We

are talking about an implicit understanding between members of the group

about where we are now and where we want to be in the future and how we are

going to get there. Once we understand the strategy, the tactics will

fall into place. Once we understand

how we intend to exploit the system, the subordination issues will fall into

place. Moreover, once we have a

strategy then having a unitary internal constraint makes a world of

sense. Where the constraint resides is

no longer an issue. We may modify our

actions accordingly but the path is understood by all. Now, finally, we are in a position to explain and

understand a conundrum that usually hooks people up and doesn’t let go – the

dilemma arising out of subordination of the local to the global. The dilemma is expressed at two levels, here is the

first. We must subordinate the current tactical constraint to the future strategic constraint. Consider for example a tactical constraint that is

the paint booth in a small engineering shop, and we want the constraint to

eventually move to the assembly area of that shop. In order to do so, we may have to forgo

maximum financial throughput per unit time on the current tactical constraint

in order to build the correct business for the future desired financial

throughput on the chosen strategic constraint. We can step this out, here is the second level. We must subordinate the current strategic constraint to the future strategic constraint. We can see exactly this in Toyota today as that

company develops hybrid engine technology and brings it to market ahead of

perceived demand (8). The development

of the Cummins Engine Company and the philosophy of the Irwin-Sweeny-Miller

families is another exceptional example of this process (9). Both of these firms leverage on the present

to create the future. The leveraging

results in lower current profit than would otherwise be possible and a

greater future (and total) profit than would otherwise be possible. In fact, we could step back a little to

contemplate how Toyoda Spinning and Weaving – a very successful firm in its

own right, chose to, and evolved into an auto manufacturer. Caspari and Caspari capture this dilemma which

occurs whenever such a new strategic constraint is selected. The dilemma is presented very nicely as a

short-run versus long-run cloud (10). Generically it looks like this;

A conflict arises, however, from the extension of

these needs. In order to have good

tactics we must exploit the current constraint. But, also in order to have good strategy we

must move the system towards the future desired strategic constraint –

otherwise our leadership decisions will not be implemented. And herein lies the dilemma; we can not

both exploit the current constraint and not exploit the current constraint

(move the system towards the strategic constraint). How can we break this dilemma? Let’s see.

In fact, if we substitute “long-run”

for “good strategy” and “short-run” for “good tactics,” then we can clearly

see the relationships.

We must not locally optimize in time – unless we are

willing to sub-optimize globally over a longer period. Moreover, our short-term results only have

significance with respect to our overall strategy. If there is no strategy then short-term

gains will be overwhelmingly attractive.

If there is a strategy and the strategy is understood by all, then the

future gains will be far more attractive. Subordination remains the key; we must subordinate

the non-constraints to the constraint of the system and we must subordinate

the tactics to the strategy of the system.

This requires good leadership. Robert Simons in Levers of Control

wrote about the need to establish a critical bridge between the disciplines

of strategy, accounting, and control (11).

He did so using 4 systems as his levers. We can extend his analogy from levers of

control to levers of profit in for-profit organizations, and levers of

success in for-cause organizations. The terms “levers of profit” and “levers of success”

highlight that we leverage the system via a constraint in the physical

system. We can leverage the system by

changes in investment and expenditure, but more importantly we can also

leverage the system by changes in policy.

In the end it is really people who offer the real leverage in these

man-made systems. Regardless of how we

leverage the system we must not forget that the fulcrum “under” the lever is

time.

We can make a quick and stunningly effective

evaluation of changes that are improvements by taking care to use the 3

fundamental measurements of throughput, inventory/investment, and operating

expense while remaining mindful of where the pivot point and the constraint

are now and indeed where we would like them to be in the future. Let’s turn our attention now to some of the broader aspects,

aspects that make all of this happen; aspects of leadership. This page supersedes one initially entitled “accounting for change,” which is included here as a

link as it is still referenced by a number of other pages. Rather than use this link, there are two

excellent sources for accounting professionals. They are; Caspari, J.

A., and Caspari, P., (2004) Management Dynamics: merging constraints

accounting to drive improvement. John

Wiley & Sons Inc., 327 pp. Corbett, T.,

(1998) Throughput Accounting: TOC’s management accounting system. North River Press, 174 pp. I originally

wrote this page because I wanted to address evaluating change without recourse

to equations – well at least not straight away. This was the rationale for the see-saw

analogy. But there was another

motive. I was “irked” that the texts

said that once we move from internally constrained to externally constrained

“any additional cash will do.” I was

concerned that if you are going to invest cash on a project then your really

want the best grade return that you can obtain – even if you have to wait a

while. Moreover, when

I wrote the original version of this page Viable Vision was little known and

even less understood. Yet the heart of

Viable Vision is exactly the high grade exploitation of the external

market. I’m sure that as the text

books arrive at new editions this necessary condition of maximising

throughput in externally constrained systems will be much better explained. Of course

Viable Vision aims at turning the top line (annual sales) into the bottom

line (net profit) in 4 years. This

seems unbelievable, but it is all a matter of strategy. If we have mediocre expectations and

mediocre strategy, then we will get mediocre results. If we have a strategy that is staged around

the breaking of a sequence of internal and external constraints while all the

time seeking high grade throughput then Viable Vision in various environments

is an absolute reality. (1) Goldratt, E. M., (1990) The haystack syndrome: sifting

information out of the data ocean.

North River Press, pg 98. (2) Goldratt, E. M., (1990) The haystack syndrome: sifting

information out of the data ocean.

North River Press, pp 96-97. (3) Caspari, J. A., and Caspari, P., (2004) Management Dynamics: merging constraints accounting to drive improvement. John Wiley & Sons Inc., pp 115, 118-119. (4) Corbett,

T., (1998) Throughput Accounting: TOC’s management accounting system. North River Press, pg 55. (5) Schragenheim, E., and Dettmer, H. W., (2000)

Manufacturing at warp speed: optimizing supply chain financial

performance. The St. Lucie Press, pg

240. (6) Caspari, J. A., and Caspari, P., (2004) Management

Dynamics: merging constraints accounting to drive improvement. John Wiley & Sons Inc., 327 pp. (7) Dettmer,

H. W., (2003) Strategic navigation: a systems approach to business

strategy. ASQ Quality Press, 302 pp. (8) Liker, J. K., (2004) The Toyota Way: 14

management principles from the world’s greatest manufacturer. McGraw-Hill, pp 71-84. (9) Cruikshank, J. L., and Sicilia, D. B., (1997)

The engine that could: 75 years of values-driven change at Cummins Engine

Company. Harvard Business School Press,

587 pp. (10) Caspari,

J. A., and Caspari, P., (2004) Management Dynamics: merging constraints

accounting to drive improvement. John

Wiley & Sons Inc., pp 261-262. (11) Simons, R., (1995) Levers of control: how

managers use innovative control systems to drive strategic renewal. Harvard Business School Press, 215 pp. This Webpage Copyright © 2005-2009

by Dr K. J. Youngman |