|

A Guide to Implementing the Theory of

Constraints (TOC) |

|||||

|

Increasing Profitability Through Increased

Productivity Everyone understands the benefit of increasing

production; we invest more money, buy more manpower, buy more machinery, and

make even more money. Right? Unfortunately not nearly right as often as we

would like it to be. In fact,

sometimes the increase in total profit is marginal at best. A more attractive alternative is to increase

productivity. That is to increase

output at constant investment, manpower, and machinery. Variable costs such as raw material will

increase in proportion to output, but operating expenses should remain the

same. Therefore the contribution to

the total profit from each additional sale is leverage against the previous

unit allocation for operating expense. A 20% increase in the productivity of a typical

manufacturing company with 30% raw material cost, 40% operating expense (all

labor and all fixed expenses) and 30% profit will produce a 46½% increase in

operating profit! A 20% increase

in productivity results in a 46½% increase in profitability!

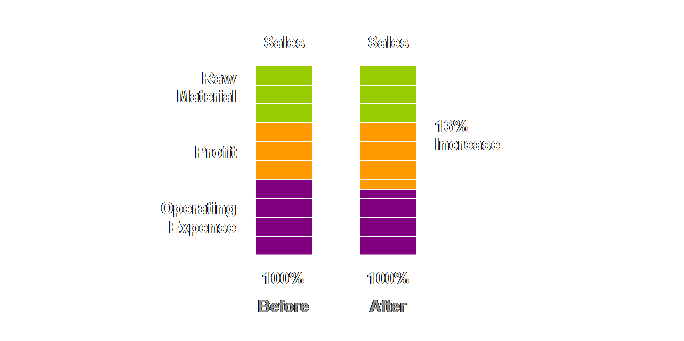

Let’s examine

the popular alternative for raising profit – cost reduction. What is the effect of a 10%

across-the-board reduction in operating expense at the current output of

100%? Attaining 10% across-the-board

would be a significant cost saving – correct?

Operating expense is 40% of the total, 10% of 40% is 4%. Therefore we save 4% of our costs and the

profit increase is therefore 4% / 30% = 13%.

Let’s draw that also.

Of course if

we chose the cost reduction way, we would have to be quite sure that our

reduction didn’t actually harm some critical function of the system in some

way. Preferences

aside, which offers greater potential for continuous improvement? Sure we can continue to cut costs, but how

much next time, another 10%? That’s

unlikely. Maybe 5%. Within a round or two the potential for

further improvement is essentially nil.

And what if sales pick up after a couple of cost-cutting rounds? In contrast

what is the potential for increasing productivity more that once? Extremely good, in fact it is open-ended, a

true pathway to continuous improvement.

Thus increasing productivity is both profitable and open-ended. One last

consideration. Many companies grow at

times by acquisition; they raise equity in the markets and acquire other

businesses in order to increase overall value through “synergies.” What we have proposed above is real organic

growth, generating robust cash inflows from which to grow the business even

more. In many places

around the world today, high growth rates are a fond memory. Indeed in some places deflation has set

in. How do we accommodate this

situation? Well, Taiichi

Ohno, the inventor of Toyota's just-in-time, once said; "In a high-growth period, productivity can

be raised by anyone. But how many can

attain it during more difficult circumstances induced by low-growth

rate? This is the deciding factor in

the success or failure of an enterprise (1).” Why, then,

aren't companies rushing out to improve their productivity &

profitability? Simply,

companies are always constrained from such growth by one of two

constraints. Either they can’t make

enough – in which case they are production constrained. Or they can’t sell enough – in which case

they are market constrained. “Few people in the world can raise productivity when production

quantities decrease. With even one

such person, the character of a business operation will be that much stronger

(1)." We have to

remove the constraints. The more

people who know how to do this, then the more companies and organizations

that can be made much stronger. Ohno

was writing about low-growth rate periods in 1978 but it is every bit as

applicable today. There are a

number of constraint classifications, but in reality there are two main

types; (1) Physical

Constraints (2) Policy

Constraints A physical

constraint, might be a resource, either a person or a machine, or a material

of some kind, time or quality, or supply issues. A policy constraint is almost everything

else that is non-tangible. Be careful, don’t be mislead into believing that

most constraints are physical – the bottlenecks that everyone seems to know

about. Physical constraints merely

become the expression of deeper underlying policy constraints. Goldratt considers that (2); "We very rarely find a company with a real

market constraint, but rather, with devastating marketing policy

constraints. We very rarely find a

true bottleneck on the shop floor, we usually find production policy

constraints. We almost never find a

vendor constraint, but we do find purchasing policy constraints. And in all cases the policies were very

logical at the time they were instituted.

Their original reasons have since long gone, but the old policies

still remain with us." If most

constraints are, in reality, policy then this should be incredibly

powerful. It means capacity in reality

already exists, we are simply holding ourselves back based upon some

internally held assumptions or convictions.

It should be possible for an organization to change its own policies,

and difficult for others to imitate.

Such conditions give rise to powerful strategic advantages which we

will address in the strategy section. In a recent major

literature survey by Mabin and Balderstone, published quantitative results

for 82 organizations were presented (3).

From this, mean values for improvement could be derived for between 30

and 32 companies. The results are

summarized as follows; Lead

time mean reduction – 70% Inventory

level mean reduction – 49% Revenue/throughput/profit

mean increase – 76% It is clear

that with the Theory of Constraints we get results. You can do the same. How quickly you obtain results depends upon

where the company is prior to starting the implementation and the company’s

ability to consistently implement the concepts, but it really does not matter

what the industry is (4). And of

course “quickly” is a relative term, and here it means several months not

several years. The revenue, or throughput, or profit increase is uniformly large

because we are using the constraint (physical or policy) to leverage against

the sunk operating expense of the organization. The greater the proportion of operating

expense, then the greater the multiplier effect of increased

productivity. Think of this as a type

of amplifier, the signal – physical output for sale – is amplified by the

sunk operating expense to generate a much greater throughput and hence

profit. Well if you

don’t sell anything to generate income for disbursement then the multiplier

effect on gross profit from operating expense won’t be there. But the potential for increase in output will

be the same none-the-less. If you do

sell something to generate a not-for-profit income – a charitable trust for

instance – then the multiplier effect will be there. For governmental agencies and similar

organizations working from funding it becomes more difficult because income

(funding) is usually capped. The

challenge still remains in these organizations, however, of how to best

increase output within existing funding. Well replace

the thought “we aren’t in manufacturing” with “we aren’t in a process.” Can you honestly say that? Most probably not. You are creating a block in your mind to

excuse yourself from drawing a synthesis from manufacturing experience into

your own non-manufacturing process.

Don’t let that happen. What about

service organizations? Think about it,

services must react quickly, so in fact there is often a lot of physical

capacity – but often it is not fully utilized. You can’t store the customers, so if they

are not there you can’t utilize the capacity.

If a service organization is constrained – it is very likely that the

constraint(s) are policy in nature and not physical. Theory of

Constraints enables for-profit organizations to substantially increase their

profitability through increases in productivity. Theory of Constraints also enables

not-for-profit organizations to substantially increase their output using

existing resources through increases in productivity. Organizations are currently blocked from

increasing output by constraints and therefore knowledge of how to surmount

such constraints is a powerful improvement methodology that has been

demonstrated to deliver substantial results. In the next

section we will take a good look at measurements and how such measurements

contribute to the current situation of poor productivity and how we can

overcome this. (1) Ohno, T.,

(1978) The Toyota production system: beyond large-scale production. English Translation 1988, Productivity

Press, pp 114-115. (2) Goldratt,

E. M., (1990) What is this thing called Theory of Constraints and how should

it be implemented? North River Press,

162 pp. (3) Mabin, V.

J., and Balderstone S. J., (2000) The world of the theory of constraints: a

review of the international literature.

St. Lucie Press, pp 11-12. (4) Stein, R. E., (1994) The next phase of

total quality management: TQM II and the focus on profitability. Marcel Dekker, pg ix. This Webpage Copyright © 2003-2009 by Dr K. J.

Youngman |